If you never planned how to leave the business, you probably never planned how to build one worth leaving.

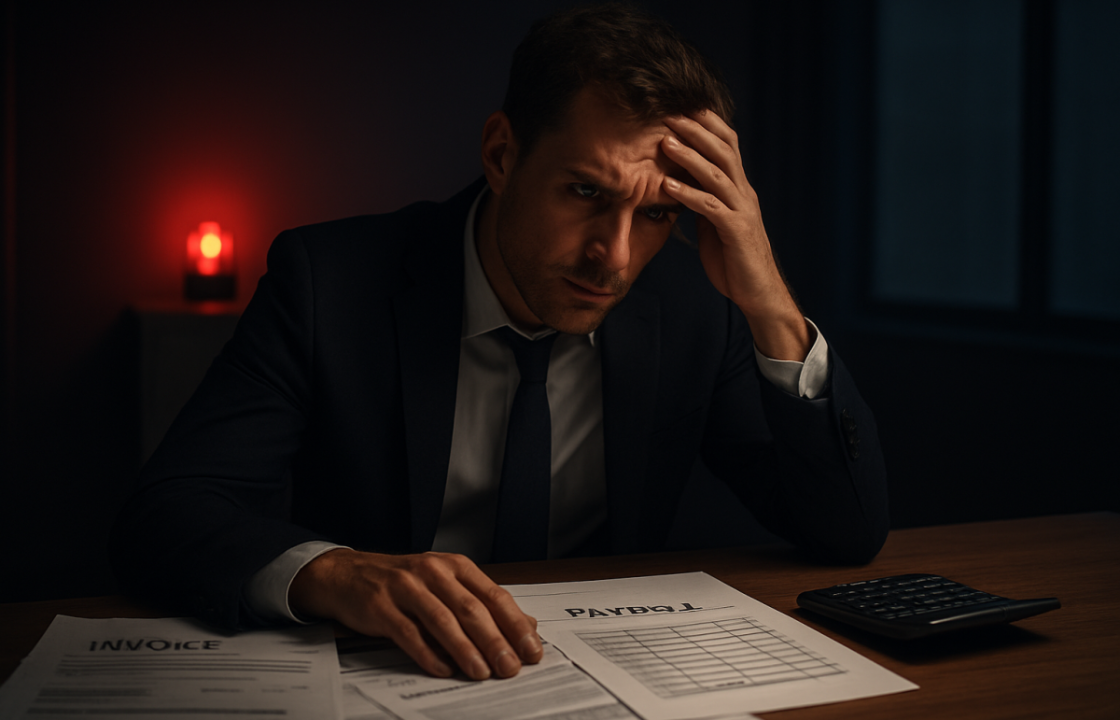

If you are using debt to patch routine cash flow, that is a Code Red. But there is a deeper problem hiding under the smoke: if you never planned how to exit the business, you probably never planned how to build it properly in the first place.

n

That sounds harsh because it is. Owners love to talk about growth, freedom, and legacy, then act surprised when the company behaves like a disorganized hobby with payroll. I have seen this pattern too many times. A business limps along, the owner is indispensable, the bank balance gets twitchy every month, and the u201cstrategyu201d is to borrow, hope, and repeat. That is not ownership discipline. That is improvisation with a filing system.

n

Money does not fix S*%$d!!! It only funds the same mess for a little longer.

n

Why exit planning belongs at the start

n

Exit planning is not about selling tomorrow. It is about deciding, from day one, what kind of asset you are trying to build. If you do not know how you want out, you will almost certainly build something that is hard to sell, hard to transfer, and hard to run without you standing in the middle of it like a traffic cone.

n

A serious owner asks early:

n

- n

- Do I want to sell, transfer, pass down, or shut this down on my terms?

- What would make this business valuable to someone other than me?

- What systems need to exist so the company can survive without my daily rescue act?

- What debt, if any, supports growth rather than panic?

n

n

n

n

n

If those questions feel uncomfortable, good. They should. Comfort is how owners drift into dependence. Dependence is how businesses become unsellable.

n

Cash flow discipline and exit discipline are the same muscle

n

Owners often treat cash flow and exit planning like separate topics. They are not. They are both about control, visibility, and repeatability. A company that cannot manage cash without emergency borrowing usually also cannot show predictable performance to a buyer, lender, or successor.

n

Think about what a future buyer sees. They do not pay for your late-night heroics. They pay for repeatable revenue, clean books, manageable staff structure, and a business that does not collapse the minute the founder takes a vacation. If every month needs a fresh loan to cover the old month, the buyer is not seeing a company. They are seeing a distress project with nicer branding.

n

That is why strategic debt has to live inside a plan. If debt helps open a profitable location, buy equipment with a measurable payoff, or support a deliberate expansion with clear returns, that is one thing. If debt is only there because the business cannot fund ordinary operations, the model is sending up flares.

n

What a business worth exiting actually looks like

n

A business worth exiting is not perfect. It is predictable. It does not depend on the owner personally remembering everything, fixing everything, and chasing every overdue invoice like a one-person recovery team.

n

Look for these signs:

n

- n

- Processes are documented, not trapped in someoneu2019s head.

- Managers make decisions without waiting for the owner to translate reality.

- Cash flow is monitored before the crisis, not after the overdraft.

- Staff roles are clear, especially where younger workers need structure, coaching, and accountability instead of vague expectations and emotional confusion.

- Debt is used with purpose, not as a daily sedative.

n

n

n

n

n

n

If that list feels basic, that is because basic is where many owners fail. Fancy growth language will not save a company that cannot run a schedule, collect receivables, or keep the team aligned.

n

Exit planning forces hard conversations

n

Most owners avoid exit planning because it forces honesty. You have to admit whether the business can stand alone, whether your staff are actually ready, whether your systems are real, and whether the company has value beyond your personal grind.

n

That honesty is useful. It tells you what to fix now, not later. It also stops the dangerous fantasy that a future sale or transfer will magically clean up years of chaos. Buyers do not buy wishful thinking. They buy evidence.

n

Exit planning is not a retirement issue. It is a management issue. If you cannot explain how the business will leave you, you probably cannot explain how it is supposed to work without you.

n

Practical steps to start today

n

You do not need a giant advisory team to begin. You need discipline.

n

- n

- Write the exit you want. Sell, transfer, pass down, or wind down. Pick a direction.

- Map the value drivers. What makes this business attractive without your presence?

- List the dependency points. Where does everything stop if you step away?

- Review debt through an exit lens. Does it create value, or does it just hide weakness?

- Fix the operating leaks. Cash discipline, staff accountability, and process control come before growth applause.

- Build the next owner test. If someone else bought this tomorrow, what would scare them off?

n

n

n

n

n

n

n

That final question is brutal, which is exactly why it works. It strips away ego. It tells you whether you have a business or a demanding job with overhead.

n

The final takeaway

n

This series has made one point over and over: if you need loans to survive routine cash flow, the business model, the operating discipline, or both are broken. Exit planning fits into that same truth. A business with no exit plan often has no real strategy, only motion.

n

So yes, plan the exit at the start. Not because you are giving up, but because you are finally acting like an owner instead of a permanent firefighter. Build something that can survive you, sell without shame, and run without monthly panic borrowing. That is what real discipline looks like.

Part 5 of 5 in this series.

#Business #Growth #Leadership #tx #ExitPlanning #CashFlow #SuccessionPlanning #SmallBusiness

Credit: This article was originally published by purpleturtlecapital.com. View the original source

Related posts:

The Real Cause of Cash Flow Crises Is Usually Inside the Business, Not in the Bank

The Real Cause of Cash Flow Crises Is Usually Inside the Business, Not in the Bank

How to Triage a Broken Business Before You Borrow Again

How to Triage a Broken Business Before You Borrow Again

If the Loan Only Buys Time, It May Be Time to Exit

If the Loan Only Buys Time, It May Be Time to Exit

Strategic Considerations Before Selling Your Business: Insights from Purple Turtle Acquisitions and Investments

Strategic Considerations Before Selling Your Business: Insights from Purple Turtle Acquisitions and Investments

Related posts

What to Fix Before You Touch a Loan Application