If you need a loan to make payroll or cover monthly gaps, the alarm is already ringing. That is not growth, that is a broken engine pretending to be a strategy.

If your company keeps running out of cash and the answer is, weu2019ll just get a loan, stop right there. That is not a growth plan. That is a code red. When a business needs borrowed money just to keep the lights on, pay suppliers, or cover payroll, the real problem is usually not the bank balance. The real problem is the engine.

And letu2019s say the quiet part out loud, because polite language helps nobody here: Money does not fix S*%$d!!! Cash can give you breathing room, but it cannot rescue a broken pricing model, sloppy collections, weak management, or a business that leaks margin like a cracked bucket.

This is part 1 of 5 in the series, and the first job is simple, separate strategic debt from survival debt. One funds a plan. The other funds denial.

What a healthy loan looks like

There is nothing sinful about debt when it is used on purpose. A proper loan supports a clear return, such as buying equipment that increases capacity, funding a specific contract, expanding into a proven market, or improving a process that reduces cost over time. In those cases, the loan is tied to an asset, a measurable outcome, or a well-tested business case.

That is strategic financing. It has a destination, a timetable, and a payback logic. You can explain it to a lender, an investor, or your own board without sounding like you are making it up on the way to the car park.

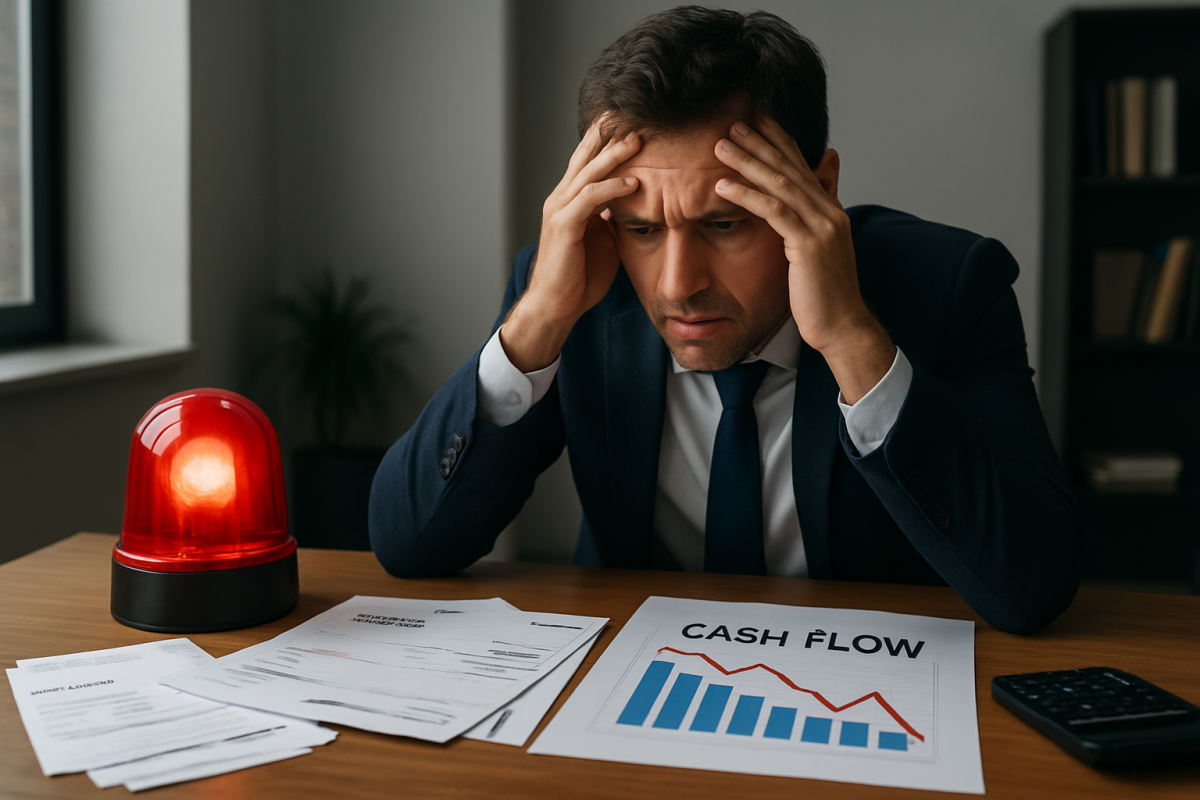

What cash flow borrowing usually means

Cash flow borrowing is different. It happens when the business is already under strain and the loan is meant to plug a hole, not fund growth. If you are using debt to survive the month, the loan is not solving the problem. It is postponing it.

That is why the phrase cash flow loan warning signs matters. The warning signs are usually obvious if you are willing to look at them without sunglasses:

- Customers pay late and collections are weak.

- Gross margins have been shrinking for months.

- Payroll, rent, taxes, and supplier payments are always a scramble.

- New sales do not seem to improve cash in the business.

- The owner is always covering gaps with personal stress and crossed fingers.

- Management spends more time firefighting than fixing root causes.

If that list feels uncomfortably familiar, good. Discomfort is useful. It means the business is telling the truth before the spreadsheet does.

How to tell the difference, fast

Ask one blunt question: Does this loan create future value, or only delay pain? If the answer is delay pain, you are not financing growth. You are borrowing time.

Here is a simple test I have used for years when reviewing SME situations:

- Define the use of funds. If the money is not tied to a specific outcome, be suspicious.

- Measure the payback source. Where exactly does the repayment come from, and when?

- Check the business model. Are you actually profitable after normal operating costs, or just busy?

- Look at discipline. Are invoices sent on time, collections followed up, stock controlled, and overheads watched?

- Ask what changed. If the business worked before but now needs constant rescue, something inside the operation changed, or was never right to begin with.

If a lender is being asked to cover recurring operating gaps, that is often a sign the business model is failing. Not u201cunder pressure.u201d Not u201cgoing through a phase.u201d Failing. There is no dignity in dressing up a broken model in fancy financing language.

Why owners reach for debt first

Most owners do not borrow because they are lazy. They borrow because they are tired, under pressure, and hoping for a clean escape hatch. I understand that. I have seen good operators make bad decisions because the fear of a missed payment feels bigger than the fear of the wrong decision.

But that is exactly how debt becomes a habit. Once the company learns it can survive by borrowing, the discipline to fix operations weakens. The pain gets hidden, not healed. And hiding a problem is not the same as solving it. It is just more expensive procrastination.

Debt should be a tactical tool, not a lifestyle choice. If the business keeps needing rescue, the rescue plan has become the business plan.

What to fix before you borrow

Before anyone signs loan papers, the owner should pressure-test the basics. Start with the obvious, because the obvious is where most businesses quietly bleed:

- Pricing: Are you charging enough to cover real costs and a fair margin?

- Collections: Are you invoicing quickly and chasing payment professionally?

- Inventory: Is cash trapped on the shelf because nobody is managing stock properly?

- Overheads: Are fixed costs growing faster than the business can support?

- Staff discipline: Is poor execution, poor attendance, or weak accountability draining output?

- Owner behaviour: Are you approving everything, fixing everything, and measuring nothing?

Often, the business does not need more cash first. It needs fewer leaks first. That is not glamorous, but neither is bankruptcy.

The hard truth owners must hear

If you need a loan to cover cash flow, treat that as a diagnostic alarm. It is the business telling you that something is broken in operations, pricing, collections, or management. Do not confuse the temporary relief of borrowed money with a real turnaround.

This is where many owners get trapped. They want the bank to play doctor. The bank is not the doctor. The bank is the oxygen mask. If the patient keeps coughing up smoke, you still have to find the fire.

The smartest move is not always to borrow. Sometimes the smartest move is to pause, cut the leak, fix the engine, and make the business capable of standing on its own legs again. That is harder than signing a loan agreement, but it is also the difference between a company that grows and a company that survives on borrowed oxygen.

Conclusion

Cash flow borrowing is not a growth strategy. It is a warning light. Strategic debt has a destination. Survival debt has an excuse. If your business needs a loan just to stay alive, do not congratulate yourself for being resourceful. Get serious about the broken system underneath.

In the next part of this series, we will look at how to identify the point where a cash flow problem stops being temporary and starts becoming a structural failure, because once you can see the break point, you can stop pretending it is a blip.

Part 1 of 5 in this series.

#Business #Growth #Leadership #tx

Credit: This article was originally published by purpleturtlecapital.com. View the original source

Related posts

Exit Planning Starts on Day One, Not at the Fire Alarm